POWER SYSTEMS |

POWER SYSTEMS |

|

|||||

| BLOG

EEE

< PREVIOUS EEE

NEXT > EV Charging Stations Across the U.S. Europe: Electricity prices in the first half of 2022 Coal 2022 - Analysis and forecast to 2025 Grid Observability For Flexibility Report Largest Pumped Storage Power Plants Technical guide - The MV/LV transformer substations EPRI: Preparing for the 2030 Energy System

< PREVIOUS EEEEEE

NEXT >

Showing 141 to 147 from 168 blogs In order to extend the content of this website, we invite you to contribute any information, including news, events, books, blog posts, universities, links, etc., you find helpful about power system engineering.

POWER SYSTEMS |

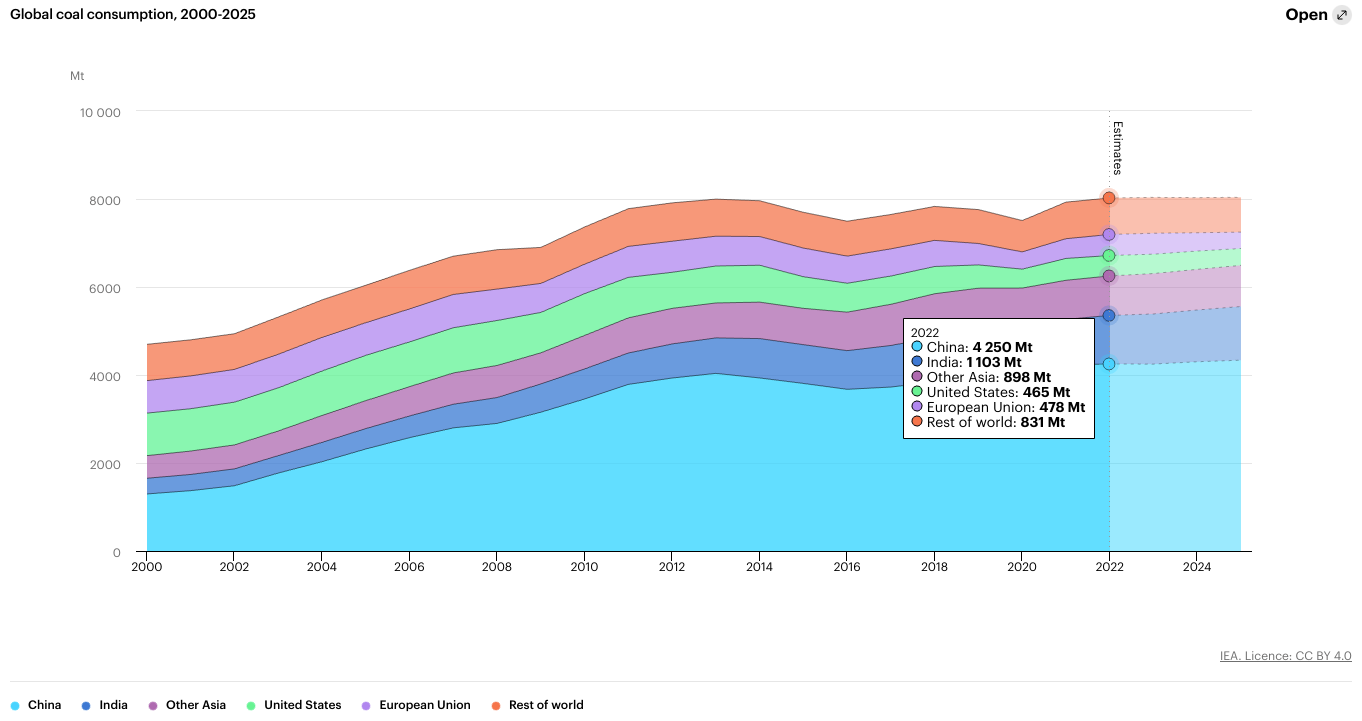

IEA - Coal 2022 - Analysis and forecast to 2025 Coal sits in the centre of climate and energy discussions because it is the largest energy source globally for electricity generation and for the production of iron and steel and of cement, as well as the largest single source of carbon dioxide (CO2) emissions. The current energy crisis has forced some countries to increase their reliance on coal in spite of climate and energy targets. Coal 2022 offers a thorough analysis of recent trends in coal demand, supply, trade, costs and prices against a backdrop of rising concern about energy security and geopolitical tensions. It also provides forecasts to 2025 for demand, supply and trade – by region and by coal grade. The report contains a deep analysis of China, whose influence on the coal market is unparalleled by any other country and in any other fuel. Download Coal 2022 - Analysis and forecast to 2025  Coal markets have been shaken severely in 2022, with traditional trade flows disrupted, prices soaring and demand set to grow by 1.2%, reaching an all-time high and surpassing 8 billion tonnes for the first time. In last year’s annual market report, Coal 2021, we said that global coal demand might well reach a new peak in 2022 or 2023 before plateauing thereafter. Despite the global energy crisis, our overall outlook remains unchanged this year, as various factors are offsetting each other. Russia’s invasion of Ukraine has sharply altered the dynamics of coal trade, price levels, and supply and demand patterns in 2022. Fossil fuel prices have risen substantially in 2022, with natural gas showing the sharpest increase. This has prompted a wave of fuel switching away from gas, pushing up demand for more price-competitive options, including coal in some regions. Nonetheless, higher coal prices, strong deployment of renewables and energy efficiency, and weakening global economic growth are tempering the increase in overall coal demand this year. In China, which accounts for 53% of global coal consumption, prolonged and stringent Covid-19 lockdowns have weighed heavily on economic activity, undermining coal demand. At the same time, droughts and heat waves in China this summer accelerated coal burning to meet a surge in power demand for air conditioning. Coal used in electricity generation, the largest consuming sector, is expected to grow by just over 2% in 2022. By contrast, coal consumption in industry is expected to decline by over 1%, mainly driven by falling iron and steel production amid the economic crisis.  Global coal power generation rises to record levels In 2022, high natural gas prices led to significant fuel switching to coal in electricity generation in Europe, although both gas and coal generation increased as the growth of wind and solar was insufficient to fully offset lower hydro and nuclear power output. In China, low hydropower output in the summer amid a big heat wave pushed coal power generation significantly higher. In August, coal power generation in China increased by around 15% year-on-year to over 500 terawatt-hours (TWh). This monthly level of generation is higher than the total annual coal power generation of any other country, except India and the United States. In India and China, where coal is the backbone of electricity systems and gas accounts for just a fraction of power generation, the impact of steeper gas prices on coal demand has been limited. Nevertheless, increased coal use in these countries has replaced some gas, which has been purchased by other regions willing to pay more for it. Coal power generation will rise to a new record in 2022, surpassing its 2021 levels. This is driven by robust coal power growth in India and the European Union (EU) and by small increases in China – and it comes despite a decline in the United States. Europe`s U-turn on coal is temporary Europe – and the European Union in particular – has been one of the regions hardest hit by the energy crisis, given its reliance on Russian pipeline supplies of natural gas. Lower hydro and nuclear power output due to weather conditions, combined with technical problems in French nuclear power plants, put additional strains on the European electricity system. In response, some European countries have increased their use of coal power generation while also accelerating the deployment of renewables and, in some cases, extending the lifetimes of nuclear plants. Under the threat of gas shortages and potential issues ensuring sufficient power system adequacy, some coal plants that had closed down or been left in reserve have re-entered the market. In most countries, this involved a limited amount of coal power capacity. Only in Germany, with 10 gigawatts (GW), is the reversal at a significant scale. This has increased coal power generation in the European Union, which is expected to remain at these higher levels for some time. But redoubled efforts to improve energy efficiency and expand renewables will see EU coal generation and demand return to a downward trajectory as soon as 2024 in our forecast. Global coal demand is set to plateau through 2025, but much depends on developments in China In our forecast, global coal demand plateaus around the 2022 level of 8 billion tonnes through 2025. However, given the current energy crisis with all its uncertainties, a lurch into growth or contraction is possible. This could be driven by changes in global economic activity, weather conditions, fuel prices or government policies – among many other potential variables. Developments in China may well have the largest impact on the outlook for global coal demand, since China accounts for more than half of it. China’s power sector alone accounts for one-third of global coal consumption. Coal consumption in China grew strongly in 2021, but growth is expected to remain relatively stagnant at an average of 0.7% a year to 2025, largely because of the increase in renewable power generation. In the 2022-2025 period, we expect China’s renewable power generation to increase by almost 1 000 TWh, equivalent to the total power generation of Japan today. Meanwhile, India’s coal consumption has doubled since 2007 at an annual growth rate of 6% – and it is set to continue to be the growth engine of global coal demand. By contrast, coal use is forecast to maintain its downward trajectory in the United States, and to fall considerably in the European Union by 2025. At a global level, we expect new renewable generation to cover almost 90% of additional electricity demand through 2025. With a modest increase in nuclear power generation and high gas prices prevailing, coal power generation increases slightly to 2025. Therefore, in the absence of low-emissions alternatives that can replace coal at scale in the iron and steel sector in the near term, global coal demand is set to remain flat through our forecast period. |